Targeted Welfare

- Share Alliance Home /

- Research /

- Targeted Welfare

More choice of services, more focused public funding

In the United Kingdom, government spending on health and social care is colossal and continues to grow as a proportion of national income. It is primarily driven by the outdated socialist mantra of universal ‘free at the point of delivery’ provision

In the United Kingdom, government spending on health and social care is colossal and continues to grow as a proportion of national income. It is primarily driven by the outdated socialist mantra of universal ‘free at the point of delivery’ provision

(image source: https://www.ukpublicspending.co.uk/healthcare_spending).

It's time to crack this seventy-year addiction. A system that handicaps targeted help to the most needy while at the same time giving free service to those who are well able to pay for their own needs cannot be described as anything other than electoral bribery.

Health spending is expected to account for £167.9 billion in 2022-23, or 41% of all central government departmental expenditure. In 2020 it was just over 7% of GDP, but it increased sharply in response to COVID-19 to over 10% of GDP in 2021.

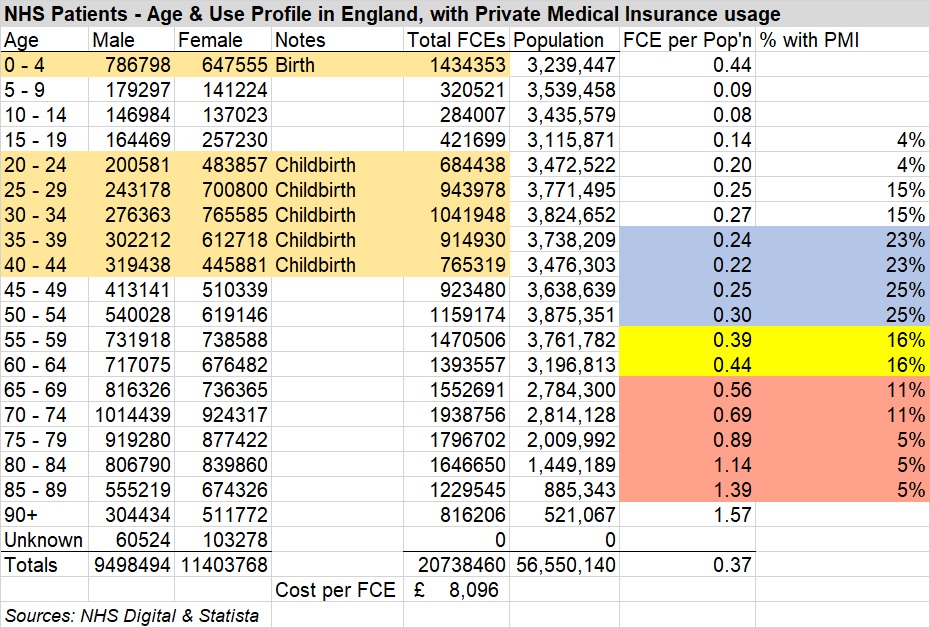

There are approximately eight million people in the United Kingdom with active private health insurance policies, accounting for c. 13% of the population; and about 53% of people say that they would like to invest in some form of health insurance scheme for their employees, or for themselves and their families. However private health insurance is primarily taken out as an employee benefit which falls away at retirement: precisely the stage when healthcare demands start to increase significantly.

Research published by Statista provides the age distribution of adults with private medical insurance throughout the United Kingdom in 2017. It shows how the percentage of cover drops from 25% in the 45-54 age group, to 16% for 55-64s, 11% for 65-74s, and then just 5% for those aged 75 and over. Precisely at the stage when the demands of healthcare costs are at their highest, the state is left carrying this burden:

Using ‘Finished Consultant Episodes’ as a yardstick and excluding birth impact, the average quantum of healthcare by annual cohort more than doubles from 140,482 for those aged up to 64 to 299,352 for those aged 65 and over; if that £167.9 billion cost is broken down on the same basis, the aggregate cost of looking after the 10 million people in these 30 years of old age is the same as looking after the 37 million aged up to 65.

Private medical insurance for those aged 70 or more is not cheap: for a relatively healthy couple it can be estimated at c. £7,500 pa. But where retirement follows a successful working life in terms of both income and capital, there is a significant proportion of the population who could reasonably be asked to carry this burden: ONS figures show that median individual wealth rises from £138,346 across ages 16-64 to £305,099 for people aged 65 and over.

Frontline services would not be affected by these arrangements, because those paying premiums would still be able to call for healthcare ‘free at the point of delivery’. But heath service accountants would be able to draw down payments from their private medical insurers to meet the costs of care for those for whom this cover was required. Greater use may well impact their premiums: so no doubt people would be encouraged to stay fit and healthy in body and mind for as long as possible.

This change would begin a transition towards individual choice in terms of health and social care. It would allow for a gradual convergence of the private and public supply of services, and targeted support could move over time to fund use of these services via insurance rather than the universal state budget. There are, of course, many national variants of this approach which would enable this transition to be researched.

Also, in terms of inter-generational fairness, this evolution towards supported choice would halt the injustice whereby young people are paying through their taxes for the health costs of those old folk who are well able to afford it.